Indicators on Mortgage Investment Corporation You Need To Know

Indicators on Mortgage Investment Corporation You Need To Know

Blog Article

Not known Incorrect Statements About Mortgage Investment Corporation

Table of ContentsSome Ideas on Mortgage Investment Corporation You Need To KnowThe smart Trick of Mortgage Investment Corporation That Nobody is Talking AboutThe Best Strategy To Use For Mortgage Investment CorporationExcitement About Mortgage Investment CorporationThe Definitive Guide for Mortgage Investment Corporation

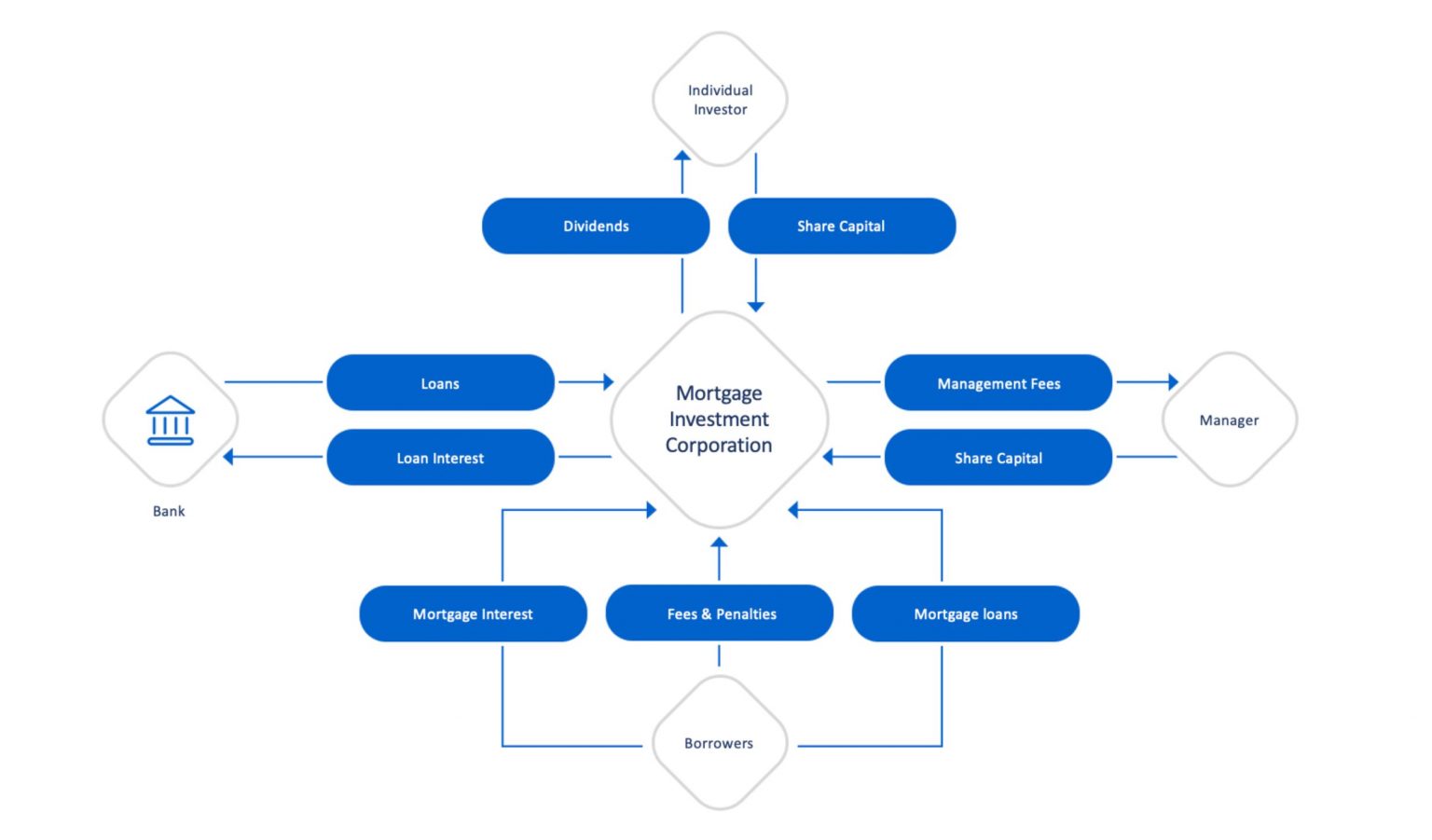

Just How MICs Source and Adjudicate Loans and What Occurs When There Is a Default Home mortgage Investment Companies supply financiers with direct exposure to the actual estate market through a swimming pool of thoroughly selected home loans. A MIC is responsible for all facets of the mortgage investing process, from source to adjudication, consisting of day-to-day management.CMI MIC Finances' rigorous credentials process enables us to take care of mortgage quality at the very start of the investment process, reducing the potential for payment issues within the loan profile over the regard to each mortgage. Still, returned and late settlements can not be proactively taken care of 100 per cent of the moment.

We spend in home loan markets across the nation, allowing us to lend throughout Canada. To find out more concerning our financial investment procedure, contact us today. Get in touch with us by completing the type listed below for additional information about our MIC funds.

Some Ideas on Mortgage Investment Corporation You Should Know

A MIC is also considered a flow-through investment vehicle, which suggests it has to pass 100% of its annual web revenue to the investors. The rewards are paid to financiers routinely, typically every month or quarter. The Revenue Tax Obligation Act (Section 130.1) details the needs that a corporation have to satisfy to qualify as a MIC: A minimum of 20 shareholdersA minimum of 50% of possessions are domestic home loans and/or cash deposits guaranteed by the Canada Down Payment Insurance Coverage Firm (CDIC)Much Less than 25% of resources for each shareholderMaximum 25% of funding spent right into real estateCannot be involved in constructionDistributions filed under T5 tax formsOnly Canadian home mortgages are eligible100% of take-home pay goes to shareholdersAnnual financial declarations investigated by an independent accountancy firm The Mortgage Investment Corporation (MIC) is a customized financial entity that spends mainly in home loan.

Furthermore, 100% of the financier's funding gets put in the picked MIC without any upfront deal charges or trailer fees. Amur Funding is concentrated on offering capitalists at any kind of degree with accessibility to professionally took care of personal financial investment funds. Investment in our fund offerings is readily available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan residents and should be made on an exclusive positioning basis.

The 5-Minute Rule for Mortgage Investment Corporation

Investing in MICs is an excellent means to gain direct exposure to Canada's thriving realty market without the needs of active building management. Apart from this, there are a number of other factors why financiers think about MICs in Canada: For those looking for returns comparable to the securities market without the connected volatility, MICs provide a secured realty investment that's easier and might be more lucrative.

Our MIC funds have traditionally delivered 6%-14% yearly returns. * MIC investors obtain dividends from the interest settlements made by borrowers to the home loan lender, developing a consistent easy earnings stream at higher rates than standard fixed-income safety and securities like government bonds and GICs (Mortgage Investment Corporation). They check out this site can also select to reinvest the dividends into the fund for compounded returns

MICs currently account for approximately 1% of the general Canadian home mortgage market and stand for an expanding sector of non-bank monetary companies. As capitalist demand for MICs expands, it is necessary to recognize just how they function and what makes them different from traditional genuine estate financial investments. MICs purchase home mortgages, not actual estate, and for that reason give exposure to the real estate market without the included danger of home ownership or title transfer.

The Greatest Guide To Mortgage Investment Corporation

generally between six and 24 months). In return, the MIC gathers Extra resources rate of interest and costs from the customers, which are after that dispersed to the fund's preferred investors as dividend payments, usually on a monthly basis - Mortgage Investment Corporation. Since MICs are not bound by numerous of the same rigid loaning needs as standard banks, they can set their very own requirements for authorizing fundings

This suggests they can charge greater rate of interest rates on mortgages than conventional banks. Home loan Financial investment Companies also delight in unique tax treatment under the Revenue Tax Function As a "flow-through" investment lorry. To prevent paying revenue tax obligations, a MIC must distribute 100% of its web earnings to shareholders. The fund should have at least 20 investors, without any shareholders owning more than 25% of the outstanding shares.

In the years where bond yields continuously decreased, Mortgage Financial investment Corporations and other alternative possessions grew in appeal. Returns have rebounded considering that 2021 as reserve banks have elevated rates of interest yet real returns remain negative family member to rising cost of living. By comparison, the CMI MIC Balanced Home loan Fund generated a net yearly yield of 8 (Mortgage Investment Corporation).57% in 2022, not unlike its performance in 2021 (8.39%) and 2020 (8.43%)

The Best Guide To Mortgage Investment Corporation

MICs, or Mortgage Financial Investment Companies, are an increasingly popular investment alternative for expanding a portfolio. MICs supply financiers with a way to spend in the realty sector without actually having physical residential or commercial property. Instead, financiers pool their cash with each other, and the MIC makes use of that money to fund home mortgages for borrowers.

That is why we want to help you make an informed choice concerning whether or not. There are many advantages linked with spending in MICs, including: Because capitalists' cash is pooled with each other and spent throughout several residential properties, their portfolios are expanded throughout different real estate types and borrowers. By owning a profile of home loans, capitalists can alleviate danger and avoid putting all their eggs in one basket.

Report this page